Report Overview

Semiconductor Back-End Equipment Market Highlights

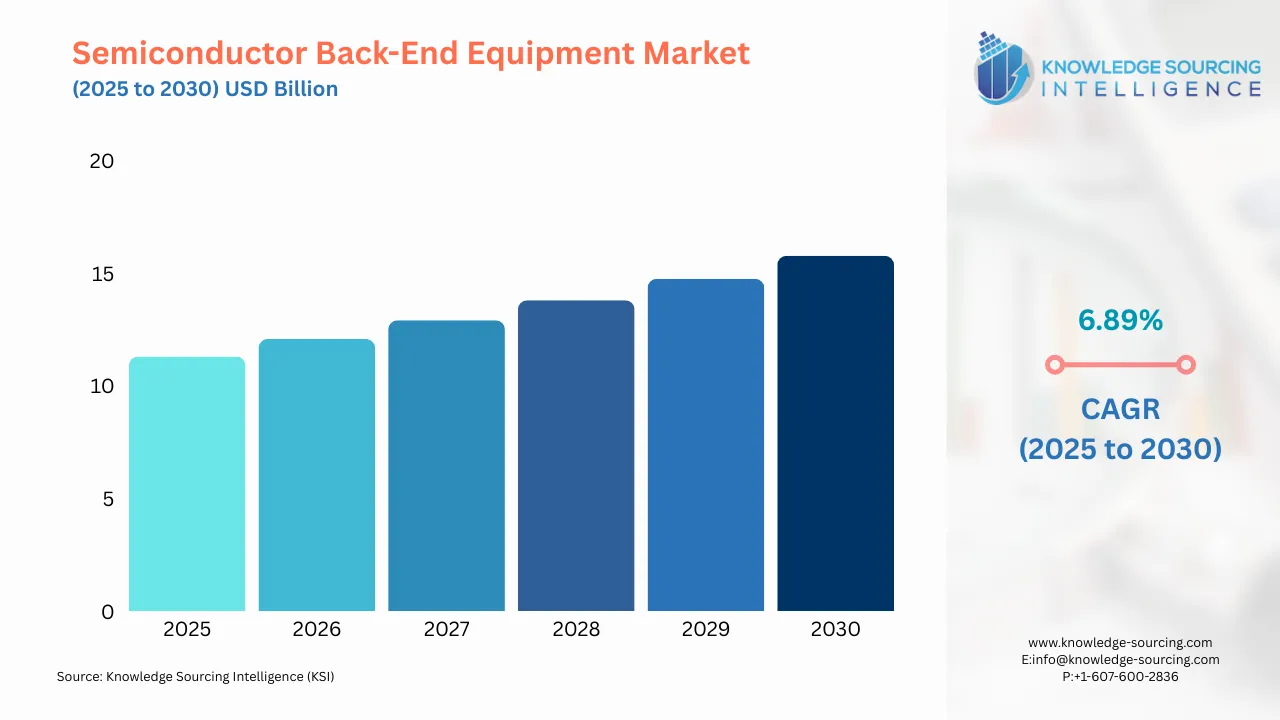

Semiconductor Back-End Equipment Market Size:

The semiconductor back-end equipment market is expected to grow at a CAGR of 6.89%, reaching a market size of USD 15.769 billion in 2030 from USD 11.301 billion in 2025.

Semiconductor Back-End Equipment Market Introduction:

The market is expected to grow due to the increasing demand for small devices and functional advancements in electronic goods like laptops, digital cameras, smartphones, and others. Since integrated circuit (IC) designs are becoming highly complex and more semiconductor products must be introduced to manufacture ICs, the demand for semiconductor back-end equipment is increasing steadily. Semiconductors are used in IC development because they lower costs, speed up mass production, and increase the operational value of the finished product.

Two processes are involved in producing semiconductors: the front-end and the back-end. Back-end processing is the step in semiconductor production that comes after the circuit definition on the wafer. Several stages are included in the processes to guarantee the functionality, dependability, performance, and durability of the semiconductor chips. Each process needs a particular set of tools to analyze and function at incredibly minute levels. Therefore, businesses provide the goods and services that semiconductor foundries and manufacturing facilities need to meet the demand for such equipment. The rising worldwide demand for semiconductors across the industrial sector has boosted their production scale, driving the semiconductor back-end equipment market.

Semiconductor Back-End Equipment Market Overview:

The semiconductor back-end equipment is used in semiconductor manufacturing, focusing on the packaging and testing of semiconductors. Hence, such equipment offers an efficient and accurate manufacturing process, thereby improving the overall speed and precision during the designing and processing operations.

The bolstering growth of electronics manufacturing is propelling the demand for high-end semiconductors used in such devices, thereby boosting the semiconductor back-end equipment market during the forecasted timeline. The National Institute of Standards and Technology, in its report, stated that in 2023, the manufacturing sector contributed about US$2.3 trillion to the GDP of the USA. In the total manufacturing sector, computer & electronic products accounted for US$299 billion, whereas machinery and electrical equipment accounted for US$152 billion and US$51 billion, respectively.

Some of the major companies include Mindteck, Kanematsu Corporation, and Canon U.S.A., Inc.

- Canon U.S.A., Inc. is a global technological service that offers products for multiple industries, like healthcare, legal, government, and education.

- Mindteck is a global information technology leader. It offers multiple technologies, like IoT, embedded systems & applications, enterprise applications & product lifecycle management, big data/analytics, and IT security, among others.

- Kanematsu Corporation is a Japanese technological leader that offers a wide range of products and solutions, like electronics & devices, ICT solutions, foods, meat & grains, and motor vehicles & aerospace, among others.

Semiconductor Back-End Equipment Market Growth Drivers:

- High demand for semiconductors

The global demand for semiconductors is increasing owing to growing end-user applications. Younger, emerging companies rely on Original Design Manufacturers (ODMs) and Outsourced Semiconductor Assembly and Test (OSAT) service providers to satisfy the demands for product development and manufacturing. Governments worldwide are focusing on domestic semiconductor production to reduce their reliance on foreign vendors. They welcome direct investment programs from well-known manufacturers and provide favorable regulations.

For instance, the Semiconductor Industry Association (SIA) announced that global semiconductor sales reached US$627.6 billion in 2024, an increase of 19.1% compared to the 2023 total of US$526.8 billion. The association further stated that the Americas region witnessed a growth of 46.3%, whereas China and Asia Pacific/all other regions witnessed a growth of 22.9% and 18.4%, respectively. Such growth in the global sale of semiconductors will positively impact the demand & usage of new wafer processing, packaging, and bonding technologies.

- Rising need in the manufacturing industry

Semiconductor wafers, IC chips, memory chips, circuits, and other components are made with semiconductor manufacturing equipment. Silicon wafer manufacturing equipment is used early in the manufacturing process. Photolithography tools, etching machines, chemical vapor deposition machines, measurement machines, and process/quality control apparatus are examples of wafer processing equipment. The semiconductor back-end equipment market is anticipated to be driven by the growing need for discrete devices, power semiconductors, and high-power modules for diverse end users. Moreover, the trend of combining semiconductors onto a single chip is growing as customers' preferences for small-sized products grow. In this case, the main application of this equipment is the assembly of semiconductor parts into a single chip.

- Increasing demand for bonding equipment

The growing need for semiconductor chips with greater efficiency, processing power, and smaller footprints is driving demand for semiconductor bonding equipment, propelling the market expansion during the forecast period.

The substantial advancements in front-end processes have also increased the need for semiconductor bonding equipment. Investments in other applications and state-of-the-art packaging technologies also fuel the need for bonding equipment solutions. In addition, producers are focusing on enhancing the semiconductors required to produce back-end machinery and semiconductor manufacturing equipment (SME).

Semiconductor Back-End Equipment Market Segment Analysis:

- The assembly packaging segment is predicted to grow robustly

The semiconductor back-end equipment market is segmented by procedure into wafer testing, bonding, dicing, metrology, and assembly and packaging. Technological innovations and the transition of advanced & microelectronics have bolstered the demand for sophisticated packaging processes such as system-in-package, fan-out wafer-level packaging, and wafer-level packaging to improve IC performance.

Moreover, this segment’s growth is triggered by massive industrial applications of semiconductor ICs, with major sectors such as electronics, automotive, and robotics emphasizing the adoption of new technological innovations.

Further, the rapid movement towards advanced packaging technologies, as well as the ever-increasing adaptations for semiconductor packaging machinery, has developed out of a necessity for smaller, faster, and more efficient semiconductors.

Additionally, one of the main factors propelling the semiconductor packaging and assembly equipment industry’s growth is the notable increase in the use and manufacturing of semiconductor chips. Additionally, the Semiconductor Industry Association (SIA) reported that sales of semiconductors worldwide reached $46.6 billion in October 2023, up 3.9% from $44.9 billion in September 2023. Packaging equipment vendors will be able to take advantage of market opportunities due to these favorable industry trends.

Semiconductor Back-End Equipment Market Geographical Outlook:

- Asia Pacific is witnessing exponential growth during the forecast period.

During the forecast period, the Asia-Pacific semiconductor back-end equipment market is anticipated to grow rapidly. Country-wise, the APAC semiconductor back-end equipment market has been segmented into China, Japan, South Korea, Taiwan, and others. Strategic investments from major domestic suppliers and the growth of the established semiconductor industry are expected to propel the market. As chip consumption rises, the Asia-Pacific semiconductor market is anticipated to more than triple in size from that of the Americas over the next four years.

Additionally, introducing 5G technology has increased demand for semiconductor chips in the region by boosting the market for equipment used in semiconductor manufacturing. It is predicted that 5G technology will significantly improve the digital infrastructure globally.

With the backing of $150 billion in funding, China is pursuing an ambitious semiconductor agenda. The nation wants to produce more chips and develop its own IC industry. Many Chinese businesses have invested in semiconductor foundries, which has heightened tensions in this vital industry where the most cutting-edge process technology is concentrated. China has made several announcements to bolster its semiconductor industry.

Moreover, the demand for back-end equipment is driven by the region's expanding semiconductor industry and growing capacity for chip production. China's tech sector wants to move up the global technology value chain by leveraging its dominant positions in electric vehicles, renewable energy, and telecommunications.

Additionally, the booming 5G infrastructure establishment, which requires high-end and precise semiconductor usage, has also paved the way for future market expansion. For instance, by the end of August 2024, China had more than 4.04 million 5G base stations, according to data from the Ministry of Industry and Information Technology. This number represented 32.1 percent of all mobile base stations in the country. In China, there are now 966 million 5G mobile users.

Further, the industry is currently concentrating on advanced semiconductors in addition to these sectors. The main forces for this shift are the memory market’s growth, active participation in the silicon carbide (SiC) race, improvements in advanced node manufacturing, and calculated investments in cutting-edge packaging and manufacturing machinery. The expanding foundry industry and investments in factories across China will also stimulate this market.

The back-end semiconductor industry has gained attention as a result of the increase in chip demand in the region's various markets. In the coming years, businesses that specialize in back-end processes will continue to make significant investments and technological advancements.

Semiconductor Back-End Equipment Market Key Launches:

- October 2025: Applied Materials introduced the Kinex™ Bonding system, the industry's first integrated die-to-wafer hybrid bonder, accelerating high-volume production of multi-chiplet packages.

- October 2025: ASML delivered the first TWINSCAN XT:260 lithography scanner for advanced packaging, quadrupling productivity for high-volume interposer and 3D integration fabrication.

- September 2025: Lam Research introduced the VECTOR TEOS 3D deposition tool, providing ultra-thick, void-free inter-die gapfill for complex 3D integration and chiplet architectures in packaging.

- September 2025: ASMPT confirmed at SEMICON West 2025 that it will showcase a full advanced?packaging portfolio (die bonders, laser dicing, plating, hybrid placement) intended for 2.5D/3D-IC and AI/HPC packaging.

List of Top Semiconductor Back-End Equipment Companies:

- Applied Materials

- Toshiba Corporation

- Kokusai Electric Corporation

- Semiconductor Equipment Corp

- Canon U.S.A., Inc.

Semiconductor Back-End Equipment Market Scope:

| Report Metric | Details |

|---|---|

| Study Period | 2021 to 2031 |

| Historical Data | 2021 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 – 2031 |

| Report Metric | Details |

| Semiconductor Back-End Equipment Market Size in 2025 | USD 11.301 billion |

| Semiconductor Back-End Equipment Market Size in 2030 | USD 15.769 billion |

| Growth Rate | CAGR of 6.89% |

| Study Period | 2020 to 2030 |

| Historical Data | 2020 to 2023 |

| Base Year | 2024 |

| Forecast Period | 2025 – 2030 |

| Forecast Unit (Value) | USD Billion |

| Segmentation |

|

| Geographical Segmentation | Americas, Europe, Middle East and Africa, Asia Pacific |

| List of Major Companies in the Semiconductor Back-End Equipment Market |

|

| Customization Scope | Free report customization with purchase |

Semiconductor Back-End Equipment Market Segmentation:

- By Procedure

- Wafer Testing

- Bonding

- Dicing

- Metrology

- Assembly Packaging

- By Geography

- Americas

- US

- Europe, the Middle East, and Africa

- Germany

- Netherland

- Others

- Asia Pacific

- China

- Japan

- Taiwan

- South Korea

- Others

- Americas